Lifetime ISA (LISA) overview

A LISA is a type of savings account. It could be suitable if you're aged between 18 and 39 and saving to buy a first home, towards your retirement or both.

Scammers are using impersonation, fake investment opportunities (including cryptocurrency), and AI-generated calls.

Skipton will never ask you to:

If you are unsure, do not proceed and contact us directly.

A LISA is a type of savings account. It could be suitable if you're aged between 18 and 39 and saving to buy a first home, towards your retirement or both.

The government will pay a 25% bonus on top of your contributions up to a maximum of £1,000 each tax year.

For example, each year you pay in up to £4,000. The government pays up to £1,000, totalling £5,000.

And our members get more.

Like exclusive offers, a say in how we're run, and extra ways to help you own a home of your own.

"The latest edition of our Skipton Group Home Affordability Index March 2026 research suggests there's green shoots of optimism for first-time buyers.

We're forecasting that buying affordability will start to improve over the next couple of years. At the end of 2025, the first-time buyer market was nearly 40% bigger than it was in 2008/09.

Opening and paying into a Skipton Cash Lifetime ISA could help you get closer to your goal of owning a home. And when you're ready to buy, we've created an innovative range of first-time buyer mortgages, that could help you get on the ladder."

Charlotte Harrison, CEO Home Financing

‡ This Property Report is not regulated by the FCA.

The Skipton Group Home Affordability Index is not a benchmark for the purposes of UK Benchmark Regulation, nor for the purposes of any other legislation or regulation. The Skipton Group Home Affordability Index is produced for information purposes only and must not be used or relied upon for commercial purposes or property related decisions. We are not responsible for any decisions made based on this information.

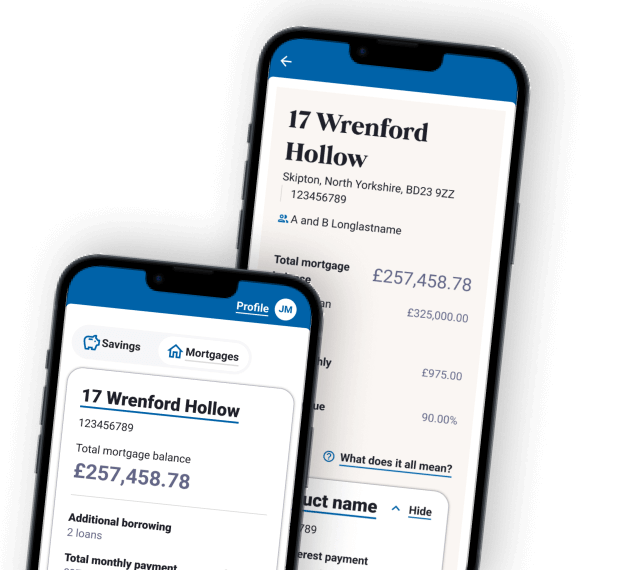

We’re gradually inviting members through our current app, so don't worry if your invite hasn't arrived yet. The new app is designed to make managing your accounts easier with a fresh look and features shaped by your feedback – plus more updates coming soon.

Find out more